Back in March, I shared my expectations on the changes in automotive value chain in next couple of years (will revisit those expectations as we got into next years to see how these shall play out.) and promised to elaborate on software and raw materials in a separate discussion. Here is a “trajet court” on the software part of EV value chain:

Autos are becoming a “software defined” vehicles. Meaning that, just similar to the smartphone migration trend over the past decade, the traditional vehicle shall possibly transform into a computing platform to support applications such as V2X, smart cockpit, entertainment and autonomous driving.

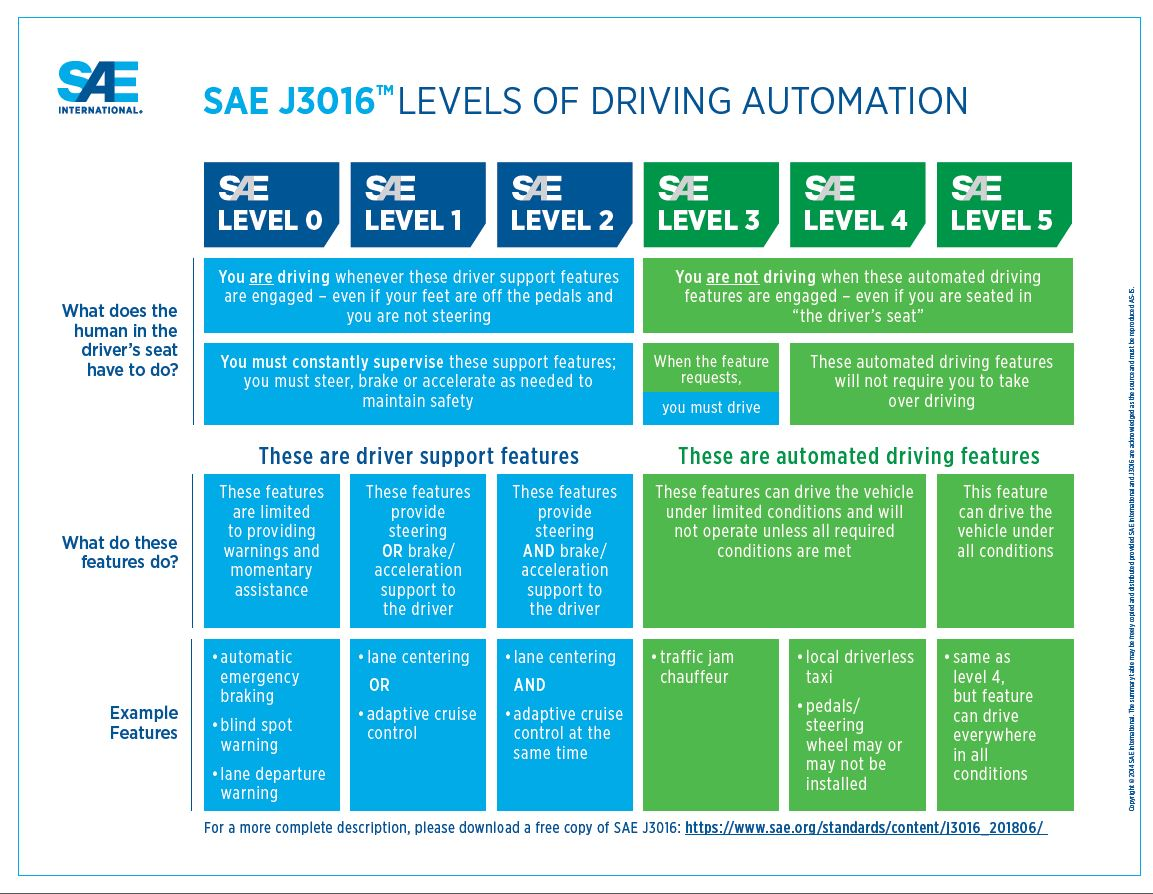

As per Society of Automotive Engineers International, diving automation is classified into 6 level, L0-L2 are considered as driving assistance (that is what the automobiles you are using right now offers to a degree) and L3+ are considered to be highly autonomous.

The autonomous driving value chain includes sensing (maps, lidar, camera), decision-making (OS, algorithms, domain controller) and execution (hardware, breaks etc.).

Structure of auto computing systems, which are critical in sensing and decision-making dimensions of the value chain, could be categorized into the following:

- Computing platform: Consists of (i) Processors: Control chips (MCU) which manages data collection, sensing and actuating, Computing chips (CPU) that executes instructions and AI Chips (GPUs or ASICs or FGPAs), power semiconductors (IGBT, MOSFET etc.) and sensor chips (TPMS etc.)

- Operating System: #Linux, #QNX, #Google or #Baidu which will oversee engine control, battery management and infotaiment

- Smart Cockpit: Voice/Speech recognition, movement recognition, gesture recognition

- ADAS: Autonomous parking, adaptive cruise control, electronic brake system, HD map integration

- Algorithm library

- Middleware

Huge competition is underway for computing platform and operating system parts as these are the backbone of auto software market and the evolution of smart cars offer huge TAM for semi and software companies.

A very good overview, I believe, on what is going on in the market was provided by Qualcomm CEO Cristiano Amon in Bernstein 38th Annual Strategic Decisions Conference (June 1, 2022):

“Well, couple of things have changed now high level, number one, I think car companies realize that they need to have a direct relationship with semiconductor companies, some of them didn’t understand what the importance semiconductor supply chain.

Number two, the market expect the car companies to be tech companies. I love to keep

bringing in this example. At some point Rivian selling hundreds of trucks was worth more

than Volkswagen. So the — what is basically saying is the companies need to be tech

companies they need digital assets. With piece number three, which is it’s not about

components from the care, but do you actually have a digital platform that they can build

on the digital platform, a lot of software assets and then apply that up and down for

different models. That’s the unique thing about the digital chassis.”

Turkish automotive suppliers and IT players including #ventures and #startups are better to have a close eye on what is going on the autonomous driving value chain to keep their shares in execution part of the chain as supplier to OEMs and (hopefully) to try to capture a share in sensing part.