Modern sanat hakkında bazen böyle hissettiğim doğrudur 🙂

Strateji, İş Geliştirme, M&A, Yönetim

Modern sanat hakkında bazen böyle hissettiğim doğrudur 🙂

Stormy weather in Istanbul gave me more time to read in the weekend. Below are the summary of the remains of the week in my notebook:

> Foodservice Recovery in the US

With its defensive characterics in staples, food distribution also benefits from growth in relatively discretionery segments.

Restaurants -%60 of the overall foodservice=$600Bn– proved to be more resilient than we thought during the pandemic: Only 11% were permenantly closed and the industry fully recovered pre-COVID level sales in 2021. Although its growth in 2022 has been entirely price-driven, greater productivity per unit is encouraging.

Point to note: Independent restaurants are 4x profitable for foodservice companies than overall restaurants channel on the back of higher penetration of private label, higher service levels and dynamic pricing.

Retail ($71Bn) is expected to be fastest growing part of the market with 7-8% growth p.a.

Travel & Leisure represents $63Bn part of the market and still down 40% vs 2019 levels! The segment is expected to grow around 3-4% p.a for the next decade.

Healthcare ($31Bn) is highly resilient and captured all of the pandemic sales losses.

Education ($34Bn) is another resilient part of the market that fully recovered to 2019 levels and expected to grow by 2-3% p.a. for the next decade.

Looking at the valuation of major players, current levels (9,5x-13,0x EV/EBITDA) are much lower than pre-pandemic levels (16,0x-21,0x) and considering M&A track-record of the major players (CYY, USFD, PFGC) looks reasonable.

> Fast-growing Apple Pay adoption is threathening PayPal

As per #Salesforce eComm data covering 1.5bn shoppers globally, global eComm has fallen 2% in November 22. UK & Ireland eComm are weakest in Europe, followed by Germany and France.

Interestingly, Apple Pay grew 59% (makes up 6% of US eComm) in November in the US while PayPal (15% of US eComm) adoption has fallen 8% yoy.

Unpleasent take for PayPal shareholders: Extremely benefited from pandemic era surge of eComm, PayPal shall possibly continue to face strong competition from Apple Pay in the next years.

> Electric Smelter Furnaces’ (ESF) advance in steelmaking

Direct Reduced Iron (DRI) is put forward as main tool for decarbonisation of steel making in Europe. Problem is that it requires high grade iron ore pellets which is rare in the proven reserves (c.3%). A solid alternative could be ESF which is tried in the pilot applications across Europe by #thyssenkrupp and #tatasteel.

ESF uses same converter (no certification changes), cheaper electrodes, creates much more slag and use a wide array of iron ore feedstock.

If ESF proves to be a preferred way to decarbonise, met coal demand deceleration could gain further monentum. Met coal producers are possibly very good examples of #valuetrap in the market.

Auto OEMs has been valued at low multiples despite their resiliently high cash flows in last 3-4 years. (Hard to understand for me!) Pandemic, #semi shortages and EV #disruption by new (and mainly Chinese) entrants have been among the reasons for investors/analysts to justify low multiples. (None is credible in my view.)

The news is that US is waking up to the EV race and Inflation Reduction Act shall possible be instrumental in this. IRA includes an array of incentives (similar to Chinese incentive scheme) for electric vehicles and clean energy investments in the US.

$7,500 EV tax credit, formally known as the clean vehicle credit, is introduced by IRA and this figure is split into two equal halves of $3,750. In order to be eligible for the new credit, vehicles and consumers must meet certain requirements:

Interestingly, The IRA also establishes an unprecedented credit for used EVs ($4,000 or up to %30 of the vehicle price, whichever is lower).

As expected, EV charger credit has been extended through 2032. The credit is available for both individual and commercial uses to help cover the cost of charging stations.

Main motivation of these incentives are to accelerate US EV factory buildout and initial feedback from OEMs showing that could be achieved. The incentive package is well-timed for OEMs as EV demand in two largest EV markets (China and Europe) has been sluggish. Even limited upside in US EV demand would offset the downside risks for EV demand and roll-out (which were exagerated in my view, as in the case with all ‘hot topics’).

OEMs are nowadays busy with securing their place in EV battery and equipment supply chain:

> Tesla and VW is trying to internalizing some of EV battery production while majority of other OEMs are building JVs with battery cell makers.

> VW and GM announced battery material JVs on cathode/procursor areas.

> Long-term agreements with miners become a common practice (STLA, Renault, GM, Ford) in last two months, securing supply for lithium, zinc and other critical raw materials.

> Tesla, GM and BMW also shown interest to enter lithium refiningas well as material recycling.

All these efforts shows to me that OEMs’ managements finally decided to put aside their waiting mode for emerging battery technologies and act on what is currently available in terms of technology and materials.

One should also act, en attendant Godot.

$stla StellantisNV.

+ YTD pricing power (will it continue in 2H?). High FCF

+ relatively slow EV rampup plans vs. comp (later margin dilution)

+ limited exposure to China vs. comp

+ lower breakeven vs. comp

– reliance on large vehicles (SUVs) in times of sky rocket oil prices

– deterioration of the auto demand in europe.

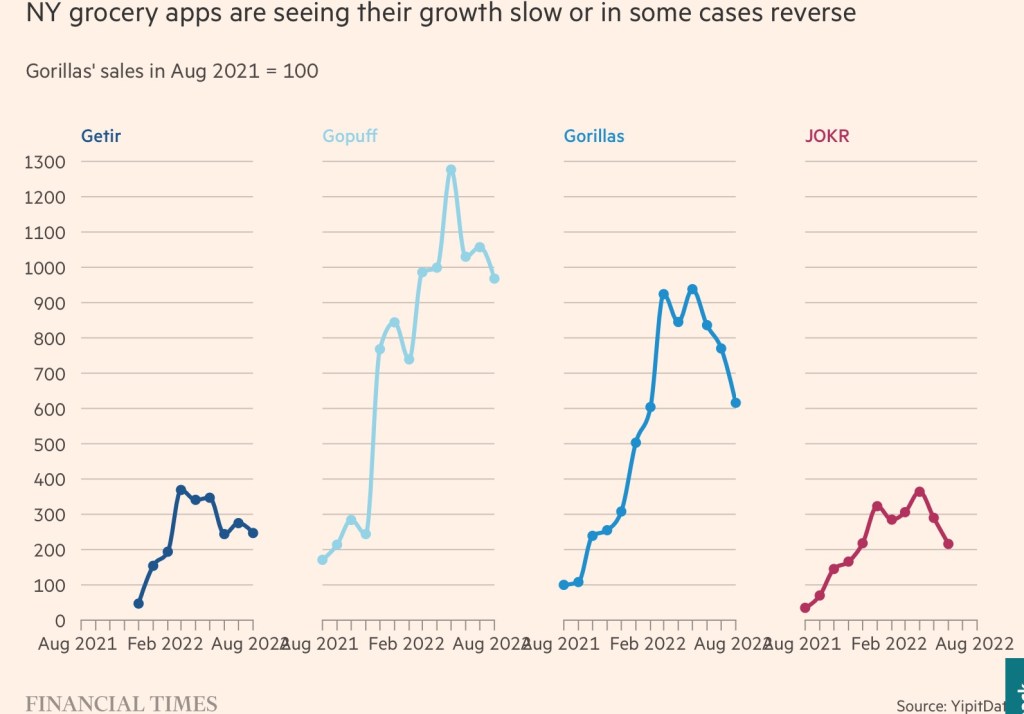

Growth by itself does not create value. If ROIC is lower than cost of capital, growth destroys value.

As there is no return in most of “#unicorns”, these are extremely successful at #value destruction.

Have a look at Gorillas: “Over the past 12 months, it was, on average, losing more than €1.50 for every €1 it generated in net revenue”

Source: Jefferies Research

Petrol fiyatları daha uzun yıllar bu seviyelerde kalabilir…

When in comes to strategy, it pays to have a closer look at the global market leaders which are -in general- the quality assets in terms of their operations, services and financials performance.

As discussed before, #Starbucks is one these with sticky and loyal customer base.

It hosted Investor Day on 9/13 at which the management surprised the market players by guiding 3-year outlook of EPS growth 15-20%, driven by investments in partners, customers and stores. The announced algoritm includes 10-12% revenue growth, global unit growth of 7% and US SSS (same store sales) 7-9% and progressive #marginimprovement.

Demand for the company’s products show no slowdown despite price incereases. Analysts argues that this achievement is closely tied to a number of factors including its sophisticated digital ecosystem, most frequent customer base in restaurants (1-2x a week), product portfolio that is difficult to replicate i.e. highly personalized product mix. The latter is also a serious challenge in terms of store productivity. Majority of the bestseller products at #SBUX (Cold Brew for instance) have labor intensive processes. This not only increases average #waitingtime by customer at the delivery desk (which is an important problem if someone is waiting you at a table or if you are just passing by a store) but also increases the pressure on the staff in the stores that are designed to fill 1,200 orders daily but actually serve around 1,500 on average.

Management is planning to leverage on the technology (#automatedordering for beverages, coffee and merchandise, #loadbalancing between stores to deal with peak hour demand, deployment of AI tools to improve wait times) and HR tools (better compensation, career planning) to deal with “good problems” they have in the system under consistently increasing demand. Will have a close eye on these fronts.

It will also be interesting to track what the management shall do for the Delivery which is a small (2% of revenues) but growing channel for the company. SBUX has an exclusive partnership with Uber Eats which shall become non-exclusive following the planned launch with DoorDash next year.

If the guidance will be achieved, SBUX could well be benchmarked with the Tech stocks in terms of growth. Comparing coffee with semiconductors or online advertisement!

Strategy is a great domain to involve.